State of Sustainability Disclosures by Indian Companies

Authors:

Aditya Kulkarni

Lakshmi Murthy

Anuradha Damle

Raghavachari Madhavan

Executive Summary

We provide an overview of the Business Responsibility & Sustainability Reporting (BRSR) data that has been disclosed by listed companies in India over FY 2022-2023 . BRSR is the equivalent framework of Environment, Social, and Governance (ESG) reporting. From 170 companies reporting in FY 2021- 2022, it has soared (by regulatory mandate) to 1,073 companies in FY 2022- 2023. We expect even more companies to disclose in FY 2023- 2024 onwards. Our focus in this report is to highlight the quantity, diversity and quality of data that has been filed, from the viewpoint of utilizing this data for investment research.

In summary, we find that there is ample room for making the data more viable for ready comparison across companies, particularly those within specific industries. The data is getting better over time, but there is a lot of room for improvement – not just validating the conformance of the report format to regulatory specifications, but also with respect to standardizing the measures that are being disclosed.

We have outlined ways in which validation and standardization of the data can be approached. Following these approaches, we have begun creating our own repository of cleansed data. In future reports, we will share results from specific investment research analysis of the cleansed data for focus industries.

Introduction

In recent years, Environmental, Social, and Governance (ESG) reporting has gained significant traction among companies globally. In India, several governmental and market regulatory agencies contribute to the governance framework mandating and overseeing BRSR disclosure/reporting including SEBI, MCA, RBI, NSE, BSE and IRDAI (see Table 1 below for their respective Role and Regulations). These regulatory bodies are working together to ensure that Indian companies not only disclose their BRSR practices but also integrate these principles into their core business strategies, thereby promoting a sustainable and responsible business environment in the country.

SEBI, fulfilling their role in governing listed securities, has taken the lead in issuing several directives for public companies to make disclosures regarding BRSR. As investors, regulators, and other stakeholders increasingly focus on sustainable practices, Indian companies are stepping up their efforts to provide transparency in their BRSR practices. However, as with any evolving field, there are challenges and inconsistencies that need to be addressed to improve the overall quality and comparability of BRSR data.

In this article we explore the extent of BRSR disclosures, and the current state of the data that is being disclosed.

Table 1: Key Agencies in Regulating ESG disclosure in India

|

Agency

|

Key Regulations

|

|---|---|

|

Securities and Exchange Board of India (SEBI)

SEBI, a primary regulatory body for securities markets in India, has introduced several guidelines and frameworks to mandate sustainability reporting among listed companies. |

|

|

Ministry of Corporate Affairs (MCA)

The MCA is responsible for regulating corporate governance and ensuring companies adhere to statutory requirements, including aspects related to social and environmental responsibility. |

National Guidelines on Responsible Business Conduct (NGRBC)

The NGRBC, which is the basis of the BRSR framework, outlines the principles and guidelines companies are expected to follow to conduct their business responsibly. Corporate Social Responsibility (CSR) The MCA mandates minimum CSR spend from profits for companies under the Companies Act, 2013. |

|

Reserve Bank of India (RBI)

The RBI, as the central bank, regulates financial institutions in India and has shown increasing interest in the integration of ESG factors into banking operations. |

Sustainable Finance:

The RBI encourages banks and financial institutions to incorporate ESG factors into their lending practices and risk management. While not a reporting mandate, the RBI's emphasis on sustainable finance influences corporate behavior in ESG matters. |

|

Stock Exchanges (NSE and BSE)

The National Stock Exchange (NSE) and the Bombay Stock Exchange (BSE) play a role in enforcing SEBI’s guidelines related to BRSR reporting among listed companies. |

Listing Requirements:

Both exchanges require companies to comply with SEBI’s BRSR and other ESG-related disclosure mandates as part of their listing obligations. |

|

Insurance Regulatory and Development Authority of India (IRDAI)

IRDAI is the regulator for Insurance companies in India. |

Sustainable Investment Practices:

IRDAI encourages insurance companies to adopt sustainable investment practices, which indirectly promotes ESG considerations in the broader market. |

As a result of the increased focus among regulators and more importantly investors, a growing number of Indian companies are now incorporating ESG data into their annual reports and sustainability disclosures. As of this writing, the Business Responsibility and Sustainability Report (BRSR) is mandatory for the top 1,000 listed companies in India based on market capitalization. These companies must file the BRSR disclosures with the Securities and Exchange Board (SEBI) of India.

However, the extent and quality of BRSR reporting can vary significantly depending on the company’s size, sector, and market capitalization. Larger firms, especially those with international operations or significant foreign investment, are more likely to have robust BRSR reporting frameworks in place. In contrast, smaller companies and those with a domestic focus may lag in this regard, either due to limited resources or a lack of perceived necessity.

Below we present our findings from an analysis of the FY2022- 2023 disclosures.

Data sources

The NSE hosts a data site under nseindia.com which holds Corporate Filings Business and Sustainability Reports as filed by public companies pursuant to the SEBI guidelines which go under the acronym BRSR (Business Responsibility and Sustainability Report) mentioned earlier. The BRSR contains general information related to the business (as such as company name, contact information, turnover, etc.) and the information pertaining to the report filing: filing date, ESG factors, their value, units reported in, and the reporting date.

The NSE also provides XBRL Filing Information which contains the taxonomy (XSD) of the factors used in BRSR required to interpret the filed reports, as well as the Excel template of the BRSR. Note that the BRSR information that NSE hosts are from FY2021- 2022. Reporting of BRSR by companies started from July 2022. Data for FY 2021- 2022 is interpreted from the taxonomy information available at this BSE Website.

Company market capitalization data was obtained from Yahoo Finance and capitalization category from AMFI.

Dates – While data is available for FY 2021-22 onwards, our focus of analysis is for FY 2022-2023. We plan to update this analysis with the FY 2023-24 as reporting is finalized.

Number of files: We located 1,254 files, with 1,073 companies reporting for FY 2022-2023

Background: Structure of BRSR

Before we report on the state of filings data, let us first review the content that is required to be filed. SEBI requires BRSR filings to contain three parts: Section A, Section B and Section C. The details of the content required in these sections are described below.

Section A provides general information about the company relevant to its business operations. This section includes details such as the company name and ID, contact information, turnover, year of reporting, operations, products and services, and employee details.

Section B focuses on the company’s environmental, social, and governance (ESG) practices. It assesses the company’s impact on the environment, its social responsibility initiatives, and its governance structures. This section aims to provide transparency regarding the company’s efforts and performance in these critical areas.

Section C includes data and information on Environmental, Social, and Governance (ESG) factors, as well as business sustainability. It is structured around nine key pillars:

- Ethics, Transparency, and Accountability

- Product Lifecycle Sustainability

- Employee Well-being

- Stakeholder Engagement

- Human Rights

- Environmental Management

- Public Policy Advocacy

- Inclusive Growth and Equitable Development

- Consumer Protection

Please refer to our article The 9 Pillars of BRSR for more details of these 9 pillars

Which Companies Are Reporting?

We start by examining the participation in BRSR filings by each Sector. We use the Global Industrial Classification Standard list of 11 sectors for all the companies under SEBI governance.

Reporting by Sector

As reported in Table 2, for FY2022- 2023, the number of BRSR reporting companies varies from a high of 215 in the Basic Materials sector to a low of 21 in the Energy sector. The growth in reporting from FY 2021- 2022 to FY2022- 2023 is highest in the Real Estate sector (a jump of 13x) and lowest in Utilities (a jump of 3x). Financial Services, Technology and Energy are also below the overall average growth ratio.

Table 2: BRSR Disclosure in India by Sector

|

Sector

|

# Companies in FY2021- 2022

|

# Companies in FY2022-2023

|

Reporting Growth Ratio

|

|---|---|---|---|

|

Basic Materials

|

32

|

215

|

7

|

|

Communication Services

|

6

|

37

|

6

|

|

Consumer Cyclical

|

26

|

184

|

7

|

|

Consumer Defensive

|

9

|

72

|

8

|

|

Energy

|

4

|

21

|

5

|

|

Financial Services

|

29

|

129

|

4

|

|

Healthcare

|

12

|

90

|

8

|

|

Industrials

|

26

|

207

|

8

|

|

Real Estate

|

2

|

26

|

13

|

|

Technology

|

15

|

64

|

4

|

|

Utilities

|

9

|

28

|

3

|

|

OVERALL

|

170

|

1,073

|

6

|

Market Capitalization Size Matters

When looking at companies by market capitalization, the disclosure rate (as a percentage of total number of companies within market cap) varies predictably, with large and mid-cap companies having over 90% disclosures in FY 2022- 2023. As reported in Table 3, there has been a considerable increase in disclosures across all categories. In large cap, the raise is almost double, in mid cap the raise is 4 times and the raise in small cap category is almost 8 times.

Table 3: BRSR Disclosure in India by Market Capitalization Level

|

Market Capitalization (number in category)

|

FY 2021-22 (% of Market Cap Category)

|

FY 2022-23 (% Market Cap Category)

|

|---|---|---|

|

Large (100)

|

44 (44%)

|

91 (91%)

|

|

Mid (150)

|

35 (23%)

|

140 (93%)

|

|

Small (5242)

|

842 (16%)

|

|

|

OVERALL (5492)

|

170 (3%)

|

1,073 (20%)

|

Note: – Total number of companies listed on BSE are 5,492 as on 23 Sep 2024.

Reporting Anomalies

Despite the progress in sustainability reporting, there are notable inconsistencies and anomalies that need to be addressed. There are discrepancies in the quality and depth of the reported data in BRSR. Some companies may provide detailed and comprehensive reports, while others might offer only a cursory overview. This variation can be attributed to differences in reporting maturity, with some firms still in the initial stages of developing their BRSR reporting capabilities. Moreover, the absence of third-party verification for many reports raises concerns about the accuracy and reliability of the disclosed information.

Key points that we will elaborate on Quality and depth of data reported are:

- PDF vs. XBRL Differences

- Challenges in utilizing BRSR reported data

- Units of data elements(metrics)

- Format changes over time

PDF vs. XBRL Differences

- XBRL provides a structured format for reporting BRSR (Business Responsibility and Sustainability Report), offering a standardized approach for data presentation. In contrast, PDF-based BRSR reports allow more flexibility, enabling the inclusion of additional details such as year-over-year analysis and highlighted points. However, there are notable differences between PDF and XBRL reporting.

- PDF file is not available on NSE. 267 companies have not created separate pdf version for BRSR on NSE. This is not a mandatory requirement under SEBI compliance. E.g. Asian Paints, Aarti Industries and Bajaj Finance have not provided the PDF.

- The structure of PDF does not match with the standard format required by BRSR. E.g., Rajesh Exports has provided a PDF with sections A to E as defined in the Business Responsibility Report instead of format for BRSR

- The Content of PDF does not include numbers that have been reported in XBRL format. E.g., ONMOBILE GLOBAL in their XBRL, reports TotalNumberOfTrainingAndAwarenessProgramsHeld for D_BoardOfDirectorsSegment as 7, but PDF document does not show any trainings for Board of Directors.

For FY 2022-23, in XBRL format, unit of a metric cannot be reported especially for Principle 6. E.g., Unit of Total energy consumption is specified only as “pure”. The actual range of units as indicated by SEBI is Joules or Multiples.

- Units of subgroups of a metric in PDF are different. To elaborate, let us take example of a metric The Total energy consumption. The Total energy consumption metric is the sum of Total electricity consumption, Total fuel consumption and Energy consumption through other resources. In the PDF file, units are different for each subgroup (and in XBRL format as “pure”). The total energy consumption (sum of all the above subgroups) is a single number in XBRL . E.g. Aster DM Healthcare has reported data in PDF and XBRL as in below table.

|

Metric

|

PDF

|

XBRL

|

|---|---|---|

|

90,039 MWh

|

90,039

|

|

|

Total fuel consumption

|

Diesel – 3,852 KL

Petrol –58 KL LPG – 242,967 Kg Firewood - 3,108,761 Kg |

3,355,638 (Sum of values in subgroups without conversion)

|

|

Energy consumption through other sources

|

Solar Energy – 3,675,000 kWh

Wind Energy – 2,300,000 kWh Hydro Energy – 3,569,298 kWh |

9,544,298- Unit can be guessed as kWh

|

|

Total energy consumption

|

Electricity – 90,039 MWh

Diesel – 3,852 KL Petrol –58 KL LPG – 242,967 Kg Firewood - 3,108,761 Kg |

12,989,975 (Sum of values in subgroups without conversion)

|

Challenges in utilizing BRSR reported data

- BRSR requires companies to report data values for metrics as an Elements. Each data value in Elements is either number or text. For FY 2022-2023, the numerical Elements reported by all companies are 612,410. Out of these 384,685 elements are values reported as 0, making up 62.8% of all values reported. The number of values not reported (blank) are negligible (766).

- Since the inception of BRSR reporting from FY 2021-22, there was inconsistency regarding which metrics to report and units associated with the metrics. E.g., Companies does not report Hazardous air pollutants, energy consumption or waste related data. Specifically, here are few instances:

- TCNS CLOTHING CO. does not record SOx.

- ABB India does not report metric PersistentOrganicPollutants or HazardousAirPollutants.

- EPL does not record metric VolatileOrganicCompounds.

- Somany Ceramics has reported waste generated in various subgroups, but does not quantify waste disposed or recovered.

- Uniphos Enterprises reported (P6- Total Energy consumption or GHG emissions) as 0.

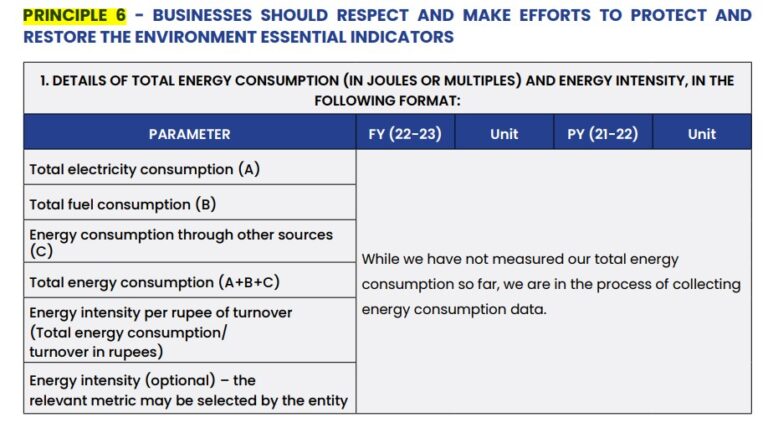

- Some companies have indicated that the process of establishing monitoring systems is in progress for certain metrics. E.g., MRF reported Volatile organic compounds(P6) as “We are in the process of establishing monitoring systems across all our plants.”, Tamilnad Mercantile Bank reported Energy Consumption(P6) as below:

- Some metrics may not be relevant to all sectors or industries. E.g., In the Financial services sector Regional Bank companies (e.g. ICICI bank, Tamilnad Mercantile Bank) reported that Air emission elements are not applicable. This should be distinguishable from not measuring or having a zero value.

- Within the same sector and industry, the critical metrics are sometimes missing from some companies while other companies have reported.

- For instance, in the Energy sector (industry -Oil & Gas Refining & Marketing), Confidence Petroleum India has reported its P6 elements as NIL or nothing (total energy consumption, waste, GHG emissions etc.) as compared to peers like Indian Oil Corporation, Hindustan Petroleum Corporation.

- Similarly, in the Financial Services sector, Punjab National Bank has reported important energy consumption (P6) related data as 0 as compared to Axis Bank, Bank of Baroda. This makes it difficult to assess their environmental impact accurately.

- Intensities (e.g., Scope1 Scope 2 emissions per turnover or Energy intensity) are not calculated and reported even though all supporting elements have been reported. E.g., Bajaj Auto has reported elements of energy consumption. But metric EnergyIntensityPerRupeeOfTurnover is reported as 0., Action Construction Equipment Limited has reported elements of energy consumption. But metric EnergyIntensityPerRupeeOfTurnover is reported as 0.

- Similarly, percentages are not calculated or wrongly calculated even though supporting elements have been reported. E.g. Pricol has reported the metric %persons covered under awareness programs as a zero though Total trainings are 371.

Units of reported Metrics

Most of the principles of BRSR (P1, P2, P3, P5, P7, P8, P9) have defined specific units for each metric to be reported. However, for principle P6, companies can define their own units for metrics such as Air Emissions, GHG Emissions, etc. We examine some of the anomalies where the reported metrics deviate from the requirement.

- In FY 2022- 2023, the unit for Energy consumption metric is “Joules or Multiples”. However, deviation from defined unit of Energy consumption is seen in some cases E.g., CITY UNION BANK and Precision Wires India have reported energy consumption in INR or multiples of INR.

Format changes over time

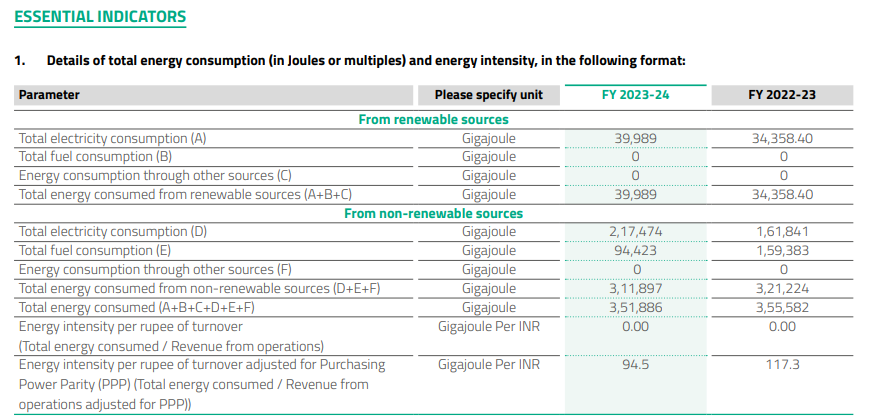

- It has been observed that the reporting format has seen some changes for FY2023- 2024. E.g., in FY 2023- 2024, the reporting format allows exact units to be accommodated. (E.g., Energy consumption). Hence the numbers can be converted to standard units for analysis.

- This has resulted in reporting numbers in varying units across different years, E.g., Energy consumption metric of Aster DM Healthcare India Ltd. has changed between FY 2022-2023 (varying units) and FY 2023- 2024(standardized as GJ) as seen below

FY 2022- 2023

|

Metric

|

PDF

|

XBRL

|

|---|---|---|

|

90,039 MWh

|

90,039

|

|

|

Total fuel consumption

|

Diesel – 3,852 KL

Petrol –58 KL LPG – 242,967 Kg Firewood - 3,108,761 Kg |

3,355,638 (Sum of values in subgroups without conversion)

|

|

Energy consumption through other sources

|

Solar Energy – 3,675,000 kWh

Wind Energy – 2,300,000 kWh Hydro Energy – 3,569,298 kWh |

9,544,298- Unit can be guessed as kWh

|

|

Total energy consumption

|

Electricity – 90,039 MWh

Diesel – 3,852 KL Petrol –58 KL LPG – 242,967 Kg Firewood - 3,108,761 Kg |

12,989,975 (Sum of values in subgroups without conversion)

|

FY 2023- 2024(from PDF)

Path Forward: Making Measures Comparable

We have outlined issues with validation and standardization of BRSR data that is reported. To improve the comparability and reliability of ESG measures across companies, a structured approach is needed for validating and standardizing data that is disclosed by the reporting companies. This involves both better reporting practices by companies and the inspection of adherence to recommended standards by regulatory bodies. Such an inspection may also involve a 3rd party that can provide a standards-adherence certification.

Here are some suggested guidelines on the approach to achieve better validation and standardization:

Best Practices for Companies

- Mapping of Universal Frameworks to BRSR: Companies with global footprint can incorporate universally accepted frameworks such as GRI or SASB to ensure consistency in metrics and disclosure. However, it should be mandatory to report data of BRSR in its required format. The compatibility mapping of BRSR elements(metrics) with international frameworks can be referred to NSE guidelines (e.g. for Air Transportation BRSR_Guide_TR.1_ Air Transportation.pdf (nseindia.com)

- Consistency Across Reporting Platforms: Ensure uniformity in reporting formats (E.g., PDF vs. XBRL) to facilitate easier comparison of data across companies and time periods.

- BRSR metrics measurement best practices: Every metric should have set of published acceptable methodologies for measurement and it should be mandated that all companies should report the methodology used.

- Regularly Update BRSR Metrics: Consistently review and update BRSR metrics to align with evolving standards and emerging trends. Ensure year-on-year consistency in reporting while incorporating new and relevant measures.

- Enhance Data Assurance and Verification: Implement internal verification processes, and for critical metrics require third-party audits for accuracy.

- Focus on Data Quality: Prioritize the accuracy and reliability of BRSR data. Aim for investment-grade data to improve the overall quality and usefulness of BRSR measurements for stakeholders.

- Leverage Technology for Better Data Management: Digitize process of gathering, managing and reporting BRSR data. Apply advanced analytics and utilize technology tools to gain better insights, streamline reporting, and ensure seamless integration.

Best Practices for Regulatory Bodies:

- Promote Adoption of Standardized Frameworks: Encourage or mandate the reporting of BRSR. BRSR framework is compatible with universally accepted ESG reporting frameworks, such as GRI, SASB, and ISSB. However, it might be beneficial to take an additional step and specify framework of metrics (sector wise) along with the best practices and methodologies of measurements. Also, provide validation tools to ensure accuracy in reporting.

- Facilitate Regular Review of BRSR Standards: Support and drive periodic reviews of BRSR metrics and standards to keep pace with evolving best practices and emerging trends.

- Ensure Comprehensive Data Verification: Set standards for rigorous mandatory internal verification processes and third-party audits to provide assurance of data integrity and prevent risk of greenwashing.

- Standardize Reporting Formats and Units: Establish guidelines for consistent reporting formats and units to eliminate discrepancies. A specific issue would be to provide a way for companies to indicate that they are intentionally leaving a metric at 0 or as a Blank – that will serve to eliminate any doubt as to whether there was an error of omission.

Conclusion

In conclusion, while ESG reporting in India has made significant strides, there is still room for progress to be made in achieving consistent, reliable, and comparable data across the corporate sector. By addressing current anomalies and adopting more standardized practices, Indian companies can enhance comparability and credibility of their BRSR disclosures. Regulatory bodies can support these efforts through clear guidelines and enforcement. This collaborative approach will provide stakeholders with the transparency they seek and contribute to a more sustainable and responsible business environment, ultimately leading to more reliable BRSR data and fostering sustainable business practices.

In our next article, we will show our innovative approach to transforming the current data to develop an understanding of overall ESG standing for each company.